Message: Return type of CI_Session_files_driver::open($save_path, $name) should either be compatible with SessionHandlerInterface::open(string $path, string $name): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::close() should either be compatible with SessionHandlerInterface::close(): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::read($session_id) should either be compatible with SessionHandlerInterface::read(string $id): string|false, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::write($session_id, $session_data) should either be compatible with SessionHandlerInterface::write(string $id, string $data): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::destroy($session_id) should either be compatible with SessionHandlerInterface::destroy(string $id): bool, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

Message: Return type of CI_Session_files_driver::gc($maxlifetime) should either be compatible with SessionHandlerInterface::gc(int $max_lifetime): int|false, or the #[\ReturnTypeWillChange] attribute should be used to temporarily suppress the notice

How to Cancel GST Registration in Bangalore & Why?

Posted on: 2019-05-24 03:43:32

There are some specific reasons as to why you can cancel the registration granted to you under GST (goods and services tax). The GST cancellation process in India can be started either by the department or by you.

In case of the department they can do so out of their own motion.

In case you – the registered person – have passed away your heirs can apply for cancellation.

If the department has cancelled your registration there is a provision that allows the cancellation to be revoked.

When you have cancelled your registration you would have to file a return. This is referred to as the final return.

So before going to cancel the registration, the taxpayer or the business owners should know the factors, understand the process and clear about the conclusion part, and then can proceed for this. To make the completed the work, hire GST consultant so they can direct you the right way and solve the problem.

It could be that you are registered under other existing laws and are thus not liable to be registered under GST

It could be that you have stopped doing the business

It could be that business owner has died and that is why the business has been fully transferred, merged with another business, demerged, or disposed of otherwise

It could be that the business is not meeting the threshold limit

It could be that a taxable person is no longer liable to be registered under the GST – please note that this does not include people who have registered voluntarily for GST under Sub section (3) of Section 25 of the CGST (central goods and services tax) Act, 2017

It could be that you have flouted the provisions and rules of the GST Act

It could be that you, who has been paying tax as per composition, have not provided returns for three straight tax periods

You are a registered person and not paying tax under composition levy – it could be that you have not provided returns for 6 straight months

It may be that even after registering voluntarily you have not started your business from a period of 6 months starting from the date when you were registered

It may be that you have obtained registration by way of fraud and intentionally suppressing or misrepresenting facts

What can be the results of cancellation?

If you cancel your GST registration you would not be needed to pay the tax anymore. In case of some businesses it is obligatory to register under GST. However, even if you cancel your registration and continue with that business it would be regarded as offence as per the rules and regulations of GST.

As a result you would have to pay some heavy fines for sure.

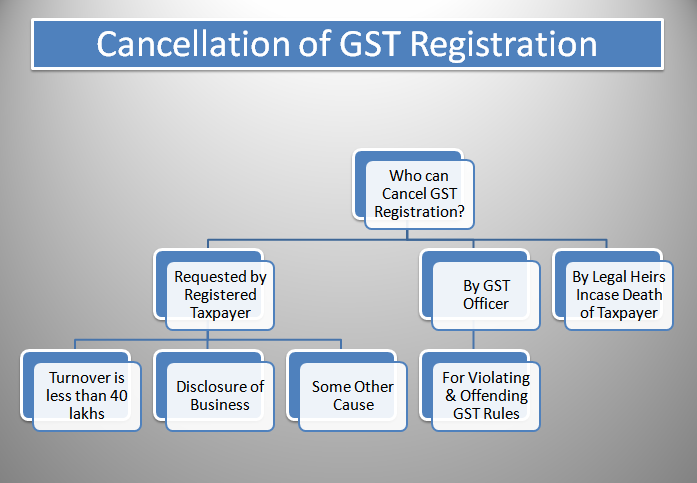

Who can cancel the GST registration?

You as the registered tax payer can request for the GST registration to be cancelled. There are various causes for which this can be done as has been stated above.

You can also do this in case your yearly turnover is less than the prescribed limit. It can also be done by the tax officer on some grounds. In case business registered person has got dead, his/her heirs can request for the same to be cancelled as well.

GST cancellation process

See the following process has to be required to get done the cancellation:

Preparation of particulars for application

File application through online

Generate ARN during application

Wait for show causes

Satisfactory reply to show cause

You’ll be asked to clear all unpaid taxes

Review by GST officer

Permission for grant of cancellation

In order to cancel the registration you need to know how to cancel GST registration. If you are already registered under existing tax laws such as central excise, service tax, and VAT (value added tax) but are not liable to be registered under GST you have to first submit an application.

This has to be done electronically within a certain date by way of the Form GST REG-29 at the official portal for cancellation. The registration would be cancelled by the Superintendent of Central Tax after conducting the required enquiry.

If you have registered under SGST (state goods and services tax) or UTGST (union territory goods and services tax) your cancellation would be done as per the process mentioned in the CGST.

If the superintendent feels that your registration should be cancelled you would be notified of the same by way of the Form GST REG-17.

You would be asked to show cause as to why your registration should be cancelled. This needs to be done within a period of 7 days starting from the date the notice was issued. If your answer is found to be a satisfactory one the officer would drop the motion and pass the order in the shape of the Form GST REG-20.

However, if your answer is not a satisfactory, one officer would reject the cancel of registration at a date that she or he deems to be fit. In this case you would be asked to clear all unpaid taxes, penalty, and interest within the due date.

In case you have applied for cancellation of registration by yourself and are indeed found to be not liable to be registered under the tax or fit enough for cancellation of registration the officer in question would issue an order. This would be done by way of the Form GST REG-19.

This would be done within a period of 30 days of you making the application. In this case you would have to pay a certain amount.

The payment would have to be made by way of electronic cash ledger or electronic credit ledger. The amount would be decided on the basis of the credit of input tax or output tax for any of the following:

Stock

Capital goods

Plant and machines

The most valuable among these would be taken into consideration. The time period in this case is the date immediately before the cancellation.

In case you are paying on the basis of capital goods and plant & machinery you would have to pay an amount that is equal to the input tax credit that you have availed on the same. However, reductions are also applicable in these cases. This would be done on the basis of percentage points that have been prescribed. The other amount that comes into consideration in this regard is the tax that is to be imposed on the transaction value of these items – this would be done in accordance with Section 15. The higher amount in this case would be taken into consideration.

Even if you have cancelled the registration you are still liable to pay the taxes and other dues that you are yet to pay from the time when your registration was active. In this case the dues could be determined after cancellation as well.

Final return regarding the cancellation

When your registration has been cancelled you would have to submit the final return. This needs to be done within 3 months from either date when the order of cancellation was issued or when the actual cancellation happened. The later date would be applicable in this case.

You would need to do this electronically by way of the Form GSTR-10. This can be done on the official portal or by way of a facilitation centre that the commissioner has notified you about. The only exceptions to this norm are an Input Service Distributor, a non resident taxable person, and a person who is paying tax as per the Composition Scheme or TDS (tax deducted at source) or TCS (tax collected at source).

Revocation of GST cancellation

It could be that your registration has been cancelled by the superintendent on her or his own and not because of an application made by you. In that case you can make an application for the cancellation to be revoked. This can be done in the shape of the Form GST REG-21. In this case you need to make the application to the deputy or assistant commissioners of central tax. This needs to be done within a period of 30 days from the date that the order of registration cancellation was served. There are two ways to do it.

You can do it directly at the official portal or

Indirectly at a facilitation centre that has been suggested to you by the commissioner;

It could be that your registration has been cancelled because you did not provide the necessary number of tax returns. In that case you would have to provide the pending returns first and then file for revocation of cancellation. You also need to pay your unpaid taxes, penalties, interests, and fines – if any – in that particular regard. In case the officers find that your application is justifiable enough and that there are enough grounds for your cancellation to be revoked they would do so.

This would be done by way of the Form GST REG-22. It would be issued within a period of 30 days of having received your application and you would be informed of the same as well. However, if they find your application to be unsatisfactory you would be issued a notice whereby you would be asked to show causes as to why your application should not be rejected. This would be done by way of the Form GST REG-23. You would need to provide the reply within 7 working days in the shape of the Form GST REG-24.

In case your clarification information is good enough the officer would follow the process as in Form 22. However, if it’s not then your application would be rejected and the Form GST REG-05 would be issued. You would be informed of the same. The process for revocation is the same across all categories of GST.

Cancel registration by expert help and support

If you want cancellation of GST registration in Bangalore; you need to get the expert help & supportto cancel registration for sure of effective on time. For this case, it is better to get expert and professional help in these matters because they can get the job done much better than what you may have managed by yourself for sure. So, we can fix your all issues related to GST matter timely.